Quiz: What's your true risk tolerance?

Share:

Answering these questions can help you get a better handle on how you really feel about the market's ups and downs and what that might mean for your investing decisions

If someone asks how comfortable you are with risk, you might immediately consider whether you're conservative by nature, have more of a go-for-it attitude or are somewhere in between. But when it comes to investing, your feelings, while they're crucial, tell only part of the story. The other major piece of the puzzle is your capacity for risk as determined by your financial situation, goals, cash needs and time horizon.

"Understanding both sides of the equation, willingness

and capacity, is useful as you seek to invest in a way that fits your overall financial picture and that feels comfortable for you," says Anil Suri, head of Asset Allocation and Portfolio Construction Analytics for the Chief Investment Office (CIO), Merrill and Bank of America Private Bank. The quiz below can help you better understand your risk tolerance, as it highlights strategies to consider — and

traps to avoid.

How comfortable are you with financial risk?

Question 1: You want to keep at least $50,000 in a certain investment account. A market dip drops the value to $45,000. What's your reaction?

Select response for insights

Tip:

Consider using tax-loss harvesting, which involves selling some stocks at a loss to offset capital gains taxes on other assets when you weed unproductive investments from your portfolio.

This positive mindset is generally suited to long-term investing. The best market days have often come on the heels of downturns.Footnote 1 And while stocks are more susceptible than bonds and cash to short-term volatility, over the long term they historically have tended to offer significantly higher returns.Footnote 1 Still, don't assume that you should hold onto every investment, no matter what. Investors who will happily sell appreciated stocks for a gain often hold onto declining ones too long for fear of realizing a loss.

Tip:

Check out the "What kind of investor are you?" slideshow at the end of this quiz for an idea of what different kinds of asset allocations might look like. A portfolio geared to your personal risk tolerance could help you stick with your strategy.

Whether it's physical exercise or investing, targets can help you measure your progress toward goals. But they have their limits. For risk-averse investors, falling below a target, even temporarily, could prompt hasty decisions and lead to selling at a loss or missing out when the market rebounds. A risk-appropriate portfolio could help you stick with your strategy. It may also help to keep in mind that

volatility is a normal part of investing, and stocks remain essential to pursuing the long-term growth you need.

One approach to consider: Replace arbitrary thresholds with ones based on your actual financial situation, taking into account your time horizon and whether you have sufficient cash in other accounts to cover spending needs and emergencies. (See "capacity" questions 3 and 4.)

Question 2: You're given two options: A) Automatically receive $20. B) Flip a coin and receive $100 — or nothing. Which do you choose?

Select response for insights

Tip:

An advisor, if you work with one, can help you better understand your feelings about risk under various scenarios and conditions.

You may be willing to accept a higher level of risk to achieve your goals. However, "risk-tolerant" and "risk-averse" aren't absolute terms; they're two ends of a spectrum. Most of us fall in the middle of that spectrum. What's more, aversion to losses often rises with the dollar amounts involved. What if, instead of $20 versus $100 or nothing, the choice was $2 million versus $10 million or nothing? Potentially losing out on $2 million might make you more likely to pass on the coin toss.

Consider this: In an investment setting, suddenly realizing you're not as risk tolerant as you thought could lead you to make hasty decisions. An advisor, if you work with one, can help you better understand your feelings about risk under various scenarios and conditions.

Tip:

Remember that a too-conservative portfolio carries its own risks, so don't abandon stocks altogether.

It's human nature to feel the pain of losses more intensely than the happiness of gains. For those with a strong aversion to risk,

understanding your emotions could help you find an investing approach you're comfortable with.

One way of managing your fear of investment loss might be to build a more diversified portfolio, balancing your stocks or stock funds with a higher proportion of bonds or bond funds offering the potential for steady income, as well as some cash and cash alternatives.

One unexpected risk to watch out for: Be aware of the potential for hidden losses. Interest on a seemingly safe cash portfolio may not keep pace with inflation, let alone provide you with future growth. In other words, a too-conservative portfolio carries its own risks, so don't abandon stocks altogether.

Now let's consider your capacity for financial risk

Question 3: Think of a specific goal that you're investing for, like saving for college or purchasing a home. How would you describe its priority?

Select response for insights

Tip:

Dollar-cost averaging, which involves investing regular amounts at specific intervals, could help you stay on a steady course toward your important goals.

Say you're putting away as much as you can to finance a child's education or that your heart is set on retiring at 60, with no intention of working longer. Goals such as these may require a more conservative approach with a balanced mix of stocks for potential growth and bonds for potential income.

One possible strategy: Remember that becoming too conservative or delaying investing over fears of volatility could impede your goals. An approach such as

dollar-cost averaging, which involves investing regular amounts at specific intervals, could help you stay on a steady course toward your important

goals.Footnote 2

Tip:

Be careful that an aggressive asset allocation for one goal doesn't expose your overall investment strategy to too much risk.

Aspirational goals give you greater flexibility when it comes to risk. Say, for example, you'd like to start your own business, and the big question is how soon you'll be able to fund it. Or perhaps you hope to travel to Europe next summer but if that doesn't happen, exploring new U.S. vacation spots wouldn't be a disaster.

One strategy to consider: For goals such as these, you might select a more aggressive asset allocation with a higher percentage of stocks, including higher-risk, potentially higher-growth investments such as small-cap stocks. But be careful that an aggressive asset allocation strategy for one goal doesn't expose your overall investment strategy to too much risk.

Question 4: Now consider your time horizon for a goal such as retirement. How much longer do you have to prepare?

Select response for insights

Tip:

A balanced, diversified portfolio, including a variety of stocks, bonds and cash, generally gives you the best chance to meet your short- and long-term needs.

Generally, you can invest more aggressively for longer-term goals. If retirement is many years away, your portfolio has more time to recover from temporary downturns. Therefore, you may want to take on greater risk with a higher proportion of stocks for growth than you'd have if your goal was right around the corner.

That said, with a high tolerance for risk you'll need to be careful not to invest

too aggressively or too heavily in illiquid stocks — that is, stocks that might be hard to sell quickly. That's true especially as you're approaching the time when you'll need the money. A balanced, diversified portfolio including a variety of stocks, bonds and cash generally gives you the best chance to meet your short- and long-term needs. As you're nearing your goal, remember to periodically review and rebalance your portfolio if necessary. If you need help, you might want to

consider working with an advisor.

Tip:

If your investing strategy has been aggressive, you might consider adjusting your asset mix to a higher degree of income-producing bonds as retirement approaches.

As "go time" approaches, investing risks become more pronounced. If you're counting on your portfolio to produce steady income for a long retirement and you're an aggressive investor with most of your assets in stocks, a sharp market downturn shortly before you retire could reduce the portfolio's ability to produce the income you'll need.

Consider this approach: Aggressive investors might consider adjusting their asset mix to a higher degree of

income-producing bonds as retirement approaches. But avoid becoming too conservative. Remember that for a retirement lasting 20 or 30 years, you'll need some exposure to stocks to help your portfolio continue to grow. An advisor can help you review and adjust your asset allocation as you get closer to retirement.

Putting it all together

Answering the above questions is a good start to helping you better understand both your risk willingness and your risk capacity. The next step is to apply what you've learned to your actual investment strategy. "Risk tolerance really comes to life when it's tied to a clear personal goal, not just as some general trait," says Suri.

What kind of investor are you?

What kind of investor are you? Conservative: Slide 1 of 5

What kind of investor are you? Moderately Conservative: Slide 2 of 5

What kind of investor are you? Moderate: Slide 3 of 5

What kind of investor are you? Moderately Aggressive: Slide 4 of 5

What kind of investor are you? Aggressive: Slide 5 of 5

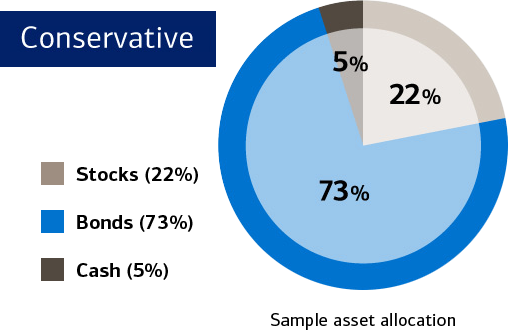

What kind of investor are you? Conservative

A sample asset allocation for a conservative investor is 22% in stocks, 73% in bonds and 5% in cash.

A sample asset allocation for a conservative investor is 22% in stocks, 73% in bonds and 5% in cash.Source: Chief Investment Office, January 2026.

The strategic allocations shown here are designed as guidelines for a 25-year investment horizon for investors with low tax sensitivity.

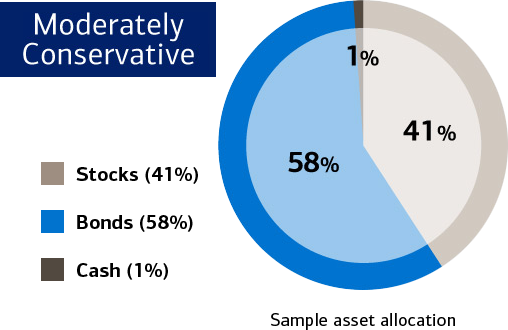

What kind of investor are you? Moderately Conservative

A sample asset allocation for a moderately conservative investor is 41% in stocks, 58% in bonds and 1% in cash.

A sample asset allocation for a moderately conservative investor is 41% in stocks, 58% in bonds and 1% in cash.Source: Chief Investment Office, January 2026.

The strategic allocations shown here are designed as guidelines for a 25-year investment horizon for investors with low tax sensitivity.

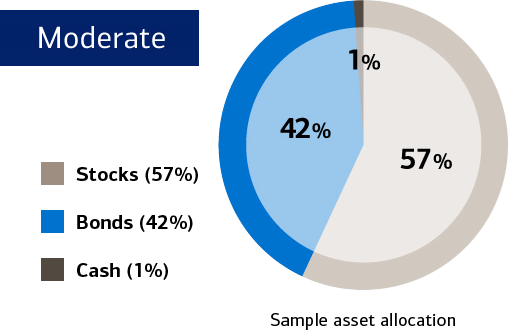

What kind of investor are you? Moderate

A sample asset allocation for a moderate investor is 57% in stocks, 42% in bonds and 1% in cash.

A sample asset allocation for a moderate investor is 57% in stocks, 42% in bonds and 1% in cash.Source: Chief Investment Office, January 2026.

The strategic allocations shown here are designed as guidelines for a 25-year investment horizon for investors with low tax sensitivity.

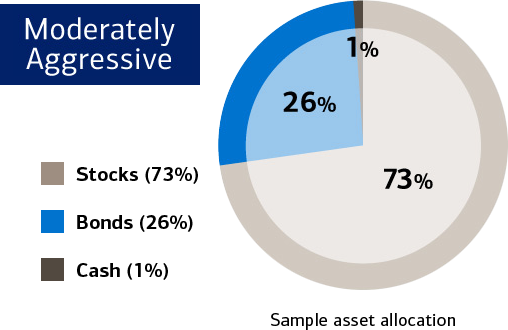

What kind of investor are you? Moderately Aggressive

A sample asset allocation for a moderately aggressive investor is 73% in stocks, 26% in bonds and 1% in cash.

A sample asset allocation for a moderately aggressive investor is 73% in stocks, 26% in bonds and 1% in cash.Source: Chief Investment Office, January 2026.

The strategic allocations shown here are designed as guidelines for a 25-year investment horizon for investors with low tax sensitivity.

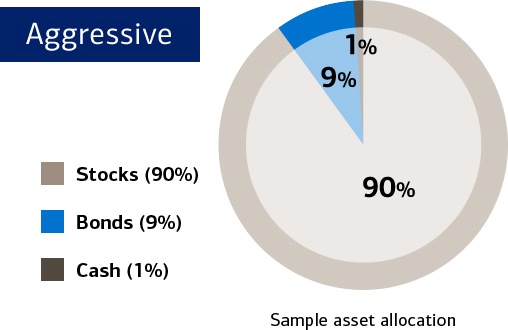

What kind of investor are you? Aggressive

A sample asset allocation for an aggressive investor is 90% in stocks, 9% in bonds and 1% in cash.

A sample asset allocation for an aggressive investor is 90% in stocks, 9% in bonds and 1% in cash.Source: Chief Investment Office, January 2026.

The strategic allocations shown here are designed as guidelines for a 25-year investment horizon for investors with low tax sensitivity.

Note: These allocations may be subject to change based on periodic review and are for illustrative purposes only. Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns.

"While you may consider yourself conservative, moderate or aggressive, the risk level that's right for you depends on a wide variety of factors," he adds.

- The amount you're investing. Your feelings on risk may fluctuate based on the dollar figures involved.

- Your goals and objectives. Understanding must-haves versus aspirational goals could help guide how you invest toward each.

- Your time horizon. More room to recover from any setbacks could let you take a bit more risk.

- Liquidity, or cash, needs. Make sure your investing approach aligns with the cash flow you need to manage your living expenses.

- How you make decisions. Are you investing on your own, or as a couple or a family? Investing strategies that respect each person's risk tolerance can help avoid potential conflict.

Investing always involves some risk. But reviewing those factors, assessing your feelings on risk and having a plan for how to respond to volatility can help you stay on track during the market's ups and downs.

Share:

Footnote 1 Merrill, "Steer the Course of Your Financial Future: A Guide for Long-term Investors," August 12, 2025.

Footnote 2 A periodic investment plan such as dollar-cost averaging does not ensure a profit or protect against a loss in declining markets. Such a plan involves continuous investment in securities regardless of fluctuating price levels; investors should carefully consider their financial ability to continue their purchases through periods of fluctuating price levels.

Important Disclosures

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

BofA Global Research is research produced by BofA Securities, Inc. ("BofAS") and/or one or more of its affiliates. BofAS is a registered broker-dealer, Member SIPC popup, and wholly owned subsidiary of Bank of America Corporation ("BofA Corp.").

Merrill, its affiliates, and financial advisors do not provide legal, tax, or accounting advice. You should consult your legal and/or tax advisors before making any financial decisions.

Asset allocation, diversification, and rebalancing do not ensure a profit or protect against loss in declining markets.

This information should not be construed as investment advice and is subject to change. It is provided for informational purposes only and is not intended to be either a specific offer by Bank of America, Merrill or any affiliate to sell or provide, or a specific invitation for a consumer to apply for, any particular retail financial product or service that may be available.

The Chief Investment Office (CIO) provides thought leadership on wealth management, investment strategy and global markets; portfolio management solutions; due diligence; and solutions oversight and data analytics. CIO viewpoints are developed for Bank of America Private Bank, a division of Bank of America, N.A., ("Bank of America") and Merrill Lynch, Pierce, Fenner & Smith Incorporated ("MLPF&S" or "Merrill"), a registered broker-dealer, registered investment adviser and a wholly owned subsidiary of Bank of America Corporation ("BofA Corp.").

All recommendations must be considered in the context of an individual investor's goals, time horizon, liquidity needs and risk tolerance. Not all recommendations will be in the best interest of all investors.

Investments have varying degrees of risk. Some of the risks involved with equity securities include the possibility that the value of the stocks may fluctuate in response to events specific to the companies or markets, as well as economic, political or social events in the U.S. or abroad. Bonds are subject to interest rate, inflation and credit risks. Treasury bills are less volatile than longer-term fixed income securities and are guaranteed as to timely payment of principal and interest by the U.S. government. Investments in a certain industry or sector may pose additional risk due to lack of diversification and sector concentration. There are special risks associated with an investment in commodities, including market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes and the impact of adverse political or financial factors.

Diversification does not ensure a profit or protect against loss in declining markets.

MAP8938693-12072027