Asset allocation is not a set-it-and-forget-it process. Over time, as some of your investments do better than others, your portfolio will naturally "drift" from your initial target allocation, favoring assets that have been experiencing stronger returns. That's why it's a good idea to revisit your portfolio regularly and see whether you need to make changes to reset it to its original proportions — a process known as

rebalancing.

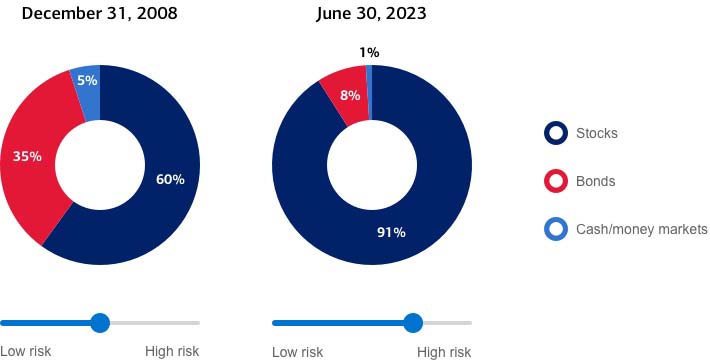

How your asset allocation could change over time

Consider a somewhat cautious investor who, at the end of 2008, chose a "moderate" level of risk for her portfolio. Even with the dramatic decline in the stock market in March 2020, by March 2023, her allocations and risk level differed from her preferred allocation. This exposes her to more risk than she's comfortable with.

Graphic that illustrates how a portfolio's asset allocation could change over time due to market returns. On December 31, 2008, the investor had a moderate level of risk with 35% in bonds, 5% in cash and 60% in stocks. On March 31, 2023, the investor had a higher level of risk with 41% in bonds, 1% in cash and 58% in stocks.

Graphic that illustrates how a portfolio's asset allocation could change over time due to market returns. On December 31, 2008, the investor had a moderate level of risk with 35% in bonds, 5% in cash and 60% in stocks. On March 31, 2023, the investor had a higher level of risk with 41% in bonds, 1% in cash and 58% in stocks.

Source: Chief Investment Office.Footnote 1 July 2023. Accessed June 2026. Strategic Asset Allocations account for impact on taxes on investment income and realized capital gains. Illustrations above are for clients with low tax sensitivity.

Periodic rebalancing can help keep your portfolio in line with your target asset allocation and the goals you want to achieve, and it can help you make more measured decisions about when to buy and sell investments, as opposed to trying to time the market. You can rebalance on a set schedule, reviewing your allocation every quarter, say, or annually — what's known as periodic rebalancing. Or you can rebalance whenever an asset strays beyond a given range — if, for example, an asset moves more than 5% from your target allocation. That's known as tolerance band rebalancing.

Over the long term, rebalancing can potentially help reduce volatility in your portfolio. An analysis by the Chief Investment Office found that from 1992 to 2020, a portfolio of 50% stocks (represented by the S&P 500 Total Return Index) and 50% bonds (represented by the Bloomberg U.S. Aggregate Total Return Bond Index) that was rebalanced annually was about 20% less volatile than a portfolio that wasn't rebalanced. Indices are used for illustrative purposes only, are unmanaged, include the reinvestment of dividends, do not reflect the impact of management or performance fees. Indices do not represent actual individual accounts. One cannot invest directly in an index.

Arriving at an asset allocation you feel is appropriate for your situation takes time and planning. But given what's at stake, that's likely time very well spent. Asset allocation is a way of instilling discipline in a part of our lives that we often find very stressful. If you can reduce that stress, it improves the odds that you will stick to your long-term goals.