Market briefs

Share:

Breaking insights on the economy, market volatility, policy changes and geopolitical events

August 5, 2026

Q2 earnings point to potential market opportunities

Could investors be in for a big letdown after a torrid first quarter for S&P 500 corporate earnings? Not according to Wall Street analysts, who project 20%-plus second-quarter year-over-year growthFootnote 1 as Q2 earnings roll in through late August.

"Two straight quarters of better than 20% growth is a high bar," says Lauren Sanfilippo, senior investment strategist in the Chief Investment Office (CIO) for Merrill and Bank of America Private Bank. "But U.S. companies continue to find ways to grow earnings." In a recent CIO Capital Market Outlook article, "

A high hurdle for Q2 earnings (PDF)," she examines what’s behind this remarkable streak and what it might mean for investors moving forward.

If analyst estimates hold, in 2026 S and P 500 companies could generate full-year, 20%-plus earnings growth for just the seventh time since 1995. Lauren Sanfilippo, senior investment strategist, Chief Investment Office, Merrill and Bank of America Private Bank. Source: Bloomberg. Data as of July 2026. Past performance is no guarantee of future results.

If analyst estimates hold, in 2026 S and P 500 companies could generate full-year, 20%-plus earnings growth for just the seventh time since 1995. Lauren Sanfilippo, senior investment strategist, Chief Investment Office, Merrill and Bank of America Private Bank. Source: Bloomberg. Data as of July 2026. Past performance is no guarantee of future results.4 good reasons for investor confidence

Though past performance is no guarantee of future results, the following statistics paint a picture of broadening market participation, says Sanfilippo.

- If analyst estimates hold, in 2026 S&P 500 companies could generate full-year, 20%-plus earnings growth for just the seventh time since 1995.Footnote 2

- Even more encouraging is the breadth of industries taking part. "All but one sector are expected to report positive Q2 earnings," she says.Footnote 3

- Stock performance has similarly broadened. While the "Magnificent Seven" tech giants rose 5.5% through mid-July, the rest of the index, "the S&P 493," rose 14%.Footnote 4

- As of mid-July, more than 60% of S&P 500 stocks were trading above their 50-day moving average, and nearly 15 were up more than 100%.Footnote 5

Sectors such as financials, healthcare and consumer staples in particular have benefited from the rotation away from a handful of mega technology stocks. Lauren Sanfilippo, senior investment strategist, Chief Investment Office, Merrill and Bank of America Private Bank.

Sectors such as financials, healthcare and consumer staples in particular have benefited from the rotation away from a handful of mega technology stocks. Lauren Sanfilippo, senior investment strategist, Chief Investment Office, Merrill and Bank of America Private Bank.Consider using the broadening market to increase diversification

"The high level of earnings growth and improving market breadth reinforces the case for portfolio diversification," Sanfilippo believes. "Sectors such as financials, healthcare and consumer staples in particular have benefited from the rotation away from a handful of mega technology stocks." Of course, conditions can change unexpectedly, but market unpredictability also argues in favor of a portfolio diversified across and within asset classes, she notes.

What's next in Q3?

Can this earnings pace continue, and what are the risks to watch out for? For ongoing insights on shifting equity market leadership, fixed income trends and portfolio strategy considerations, tune in to the CIO’s

Market Update audiocast series.

Footnote 1 FactSet as of July 8, 2026.

Footnote 2 Consensus estimate for 2026. Bloomberg. Data as of July 2026.

Footnote 3 FactSet as of July 29, 2026.

Footnote 4 Morningstar, "4 charts on the not-so-magnificent seven," July 15, 2026.

Footnote 5 Bloomberg. Data as of July 8, 2026.

July 29, 2026

Fed doesn't budge on rates: What it means for you

The Federal Reserve (The Fed) on July 29 kept its federal funds rate at 3.50% to 3.75%. While rate expectations have broadly shifted from cuts to potential increases later this year, the Fed so far this year has held steady as it processes complex and sometimes mixed signals on the economy and inflation.

What's next for interest rates?

Testifying before Congress on July 14, new Fed Chair Kevin Warsh underscored the Federal Open Market Committee's commitment "to put these years of high inflation behind us."Footnote 1 With the Iran war elevating energy costs and U.S. companies and consumers showing remarkable resilience, many analysts believe the Fed will soon raise rates to keep inflation from reigniting. BofA Global Research now expects three rate increases of .25% each in 2026, starting in September.

Yet the Fed still faces a delicate balance. Lower-than-expected inflationFootnote 2 and employment figuresFootnote 3 from June offered reminders of early 2026, when a seemingly slowing economy raised expectations of a cut. "Further rate decisions will be based on the Fed's analysis of the latest information as it unfolds," says Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank.

How can investors manage rate uncertainty?

"A period of higher rates, if it happens, could add income potential for bond investors, while making borrowing for large purchases more expensive," Hyzy notes. "But keep in mind that, wherever rates head next, one of the best ways to prepare is a well-diversified portfolio designed to pursue your personal goals."

Check back here for updates on interest rates and markets, and tune in regularly to the

Market Update audiocast for latest insights from the Chief Investment Office.

Footnote 1 The Federal Reserve, "Semiannual monetary policy report to the Congress," July 14, 2026.

Footnote 2 The Wall Street Journal, "Inflation slowed to 3.5% in June, as Americans got a break from gasoline prices," July 14, 2026.

Footnote 3 CBS News, "Employers added 57,000 jobs in June, far below forecasts as hiring slowed," July 2, 2026.

July 2, 2026

The United States: Most successful startup ever?

In nearly 1,400 words, The Declaration of Independence never uses the terms "business," "entrepreneur" or "capital investment." "Yet the founders in 1776 didn't just declare national sovereignty. They unleashed the greatest startup in history—the U.S. economy," says Joe Quinlan, head of Market Strategy for the Chief Investment Office (CIO) for Merrill and Bank of America Private Bank.

"Despite headline-grabbing challenges, the U.S. remains the world's biggest economic engine and most dynamic entrepreneurial culture," notes Quinlan, co-author of a recent CIO Capital Markets Outlook report, "

America at 250 (PDF)." The report examines "the entrepreneurial DNA of 1776," plus 10 reasons for optimism today. It's part history lesson, part investment guide and part birthday card to a nation sometimes preoccupied with its problems.

Legacy of innovation

To be sure, many of the issues we face today — polarization, geopolitical threats, economic inequality and rising debt — would trouble founders like George Washington, Alexander Hamilton and Ben Franklin, Quinlan believes. "But they'd be amazed and gratified to see that the American spirit of problem-solving and innovation lives on. Franklin, the original American entrepreneur, would be right at home with artificial intelligence (AI) and biotechnology," he says.

Reasons to celebrate

Well into the 21st century, the U.S. leads the way in industries as diverse as aerospace, agriculture, finance and health care. "With just 4% of the world's population, Americans generate roughly a quarter of its GDPFootnote 1," Quinlan says. What's the secret? Here are some of CIO's 10 reasons to celebrate:

- Geography as a superpower: Energy, minerals, waterways and arable land, plus oceans and allies at its borders, create a huge U.S. geographical edge from sea to shining sea.

- Technological prowess. "Despite China's astonishing progress in AIFootnote 2 and other technologies, the U.S. remains the largest market for R&D and innovation," Quinlan says.

- Creative destruction: Businesses rise and fall quickly, making way for fresh shoots of innovation, with nearly 6 million new business applications just in 2025.Footnote 3

- Foreign capital: Overseas investors remain bullish on the U.S., currently holding some $50 trillionFootnote 4 in U.S. Treasurys, corporate bonds, stocks and other assets.

Did you know?

- The U.S. is home to 9 of the top 10 global brands.Footnote 5

- 56.8% of global central bank holdings are in U.S. dollars.Footnote 6

- 26 of the world's 100 top-ranked universities are U.S.-based.Footnote 7

Investing in the next 250 years

"A dynamic, entrepreneurial economy goes hand-in-hand with solid equity returns," Quinlan says. "U.S. stocks should be a bedrock of portfolio construction, in our view." Yet creative destruction, while a strength, underscores the importance of diversifying across industries and sectors, with international equities and fixed income for balance. He adds, "Diversification and staying invested through short-term volatility could help position you for potential long-term growth as the U.S. economy embarks on the next era in its remarkable history."

Footnote 1 McKinsey & Company, "Sustaining America's competitive edge," May 6, 2026

Footnote 2 The Wall Street Journal, "China Has Matched Anthropic in Cybersecurity, Resetting AI Race," June 27, 2026

Footnote 3 Finder.com, "New business statistics: 2005 to June 2026," Jun 10, 2026

Footnote 4 U.S. Commerce Department and International Monetary Fund

Footnote 5 Kantar BrandZ, "Most Valuable Global Brands 2026," 2026

Footnote 6 Visual Capitalist, "Ranked: The World's Biggest Reserve Currencies Today," June 11, 2026

Footnote 7 QS Quacquarelli Symonds Limited, "QS World University Rankings 2026," 2026

June 17, 2026

Rates hold firm, for now, under new Fed chair

In Kevin Warsh's first meeting as Fed Chair, the Federal Reserve (the Fed) on June 17 held the federal funds rate steady at 3.50% to 3.75%. The decision dashed any hopes that a change in leadership might prompt immediate rate-cutting and signaled that inflation is at least as big a concern for the Fed right now as stimulating economic growth. Just a week earlier, May's Consumer Price Index (CPI) showed the annual inflation rate climbing above 4% for the first time in three years.Footnote 1

What's behind the Fed rate decision?

"Conditions have shifted from the start of the year, when two cuts for 2026 seemed likely," says Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank. The Iran war spiked energy costs and pushed prices for other goods higher, and the U.S. economy has shown remarkable resilience, adding 172,000 jobs in May.Footnote 2 Equity markets, despite heightened volatility, continue to find new highs, and long-term bond yields have risen amid investor concerns over the Middle East and inflation.Footnote 3

When could we see a rate cut?

The administration supported Warsh as likelier than his predecessor, Jerome Powell, to push for lower rates,Footnote 4 which make borrowing easier and tend to stimulate hiring. Yet sticky inflation generally prompts the Fed to do the opposite, raising rates to slow the economy. "BofA Global Research now foresees no new rate cuts until at least mid-2027, and the chances of a .25% increase in the next year have grown," Hyzy says. "Moving forward, new economic data will be the most important factor as the Fed balances its dual mandates of full employment and stable inflation."

How can you respond to periodic volatility?

May's healthy jobs numbers, while good news for workers and the economy, helped drive a 2.6% drop in the S&P 500 index on June 5 as hopes of a rate cut diminished.Footnote 5 "Investors should expect that sort of choppiness over the next few months," Hyzy believes. "Yet the job gains, spread across healthcare, logistics, financial services, hospitality and leisure and other industries, reflect strong economic fundamentals," Hyzy adds. "Stay diversified and consider viewing short-term volatility as a potential opportunity to strategically add to your portfolio," he suggests.

For bond investors, higher yields offer the potential for meaningful income. "Instead of trying to predict exactly when interest rates and yields may change, explore adding bond duration gradually and emphasizing quality," Hyzy says. Investors concerned about inflation might consider Treasury Inflation-Protected Securities (TIPS), while high-income investors concerned about taxes may find income opportunities with tax-advantaged municipal bonds.

Check back here for updates, and tune in regularly to the

Market Update audiocast from the Chief Investment Office as interest rates and inflation data evolve.

Footnote 1 CNBC, Consumer prices rose 4.2% annually in May, highest in three years

Footnote 2 The Wall Street Journal, "May jobs growth puts U.S. on a strong hiring streak," June 5, 2026.

Footnote 3 CNBC, "Treasury yields edge higher as traders weigh rate outlook, fresh Iran tensions," June 8, 2026.

Footnote 4 CNBC, "Kevin Warsh sworn in as Fed chair as Trump seeks interest rate cuts," May 22, 2026.

Footnote 5 The New York Times, "Stocks slide as investors see rates rising after strong jobs data," June 5, 2026.

May 29, 2026

The biggest oil shock: Market resilience

Latest talks between Iran and the U.S., if they succeed, could lead to a welcome opening of the Strait of Hormuz. The shutdown has caused history's greatest oil disruption, affecting some 20% of the world's supply.Footnote 1 So, how has the world thus far avoided an economic crisis? "While higher oil prices and inflation are creating real pain for millions of consumers, several factors have helped to limit its global impact so far," says Ariana Chiu, investment strategist in the Chief Investment Office (CIO) for Merrill and Bank of America Private Bank.

Which countries are most affected by the oil disruption?

"A robust economy and energy self-sufficiency are supporting U.S. economic stability in the face of the Hormuz oil shock," Chiu says. Asia, which accepts more than 80% of the oil that moves through the Strait of Hormuz,

Footnote 2 and Europe, which sources much of its jet fuel via the passageway, are feeling the brunt, she adds. Yet the global economy has shown surprising resilience, thanks to several forces that together are mitigating about half of the disrupted supply. A recent CIO Capital Market Outlook report, "

No two oil shocks are created equal (PDF)," explores those forces as well as the risks that could lead to a wider economic crisis.

What has limited its global impact so far?

Chiu points to five key factors helping the global economy weather the oil disruption:

- A prewar "super glut." Robust 2025 production created an oil oversupply of about 3 million barrels per day at the outset of the conflict.Footnote 3

- Rerouting. While the Strait of Hormuz remains a key oil conduit, exporters have offset about 5 million barrels a day using alternative pipelines and ports,Footnote 4 Chiu says.

- Strategic reserve releases. In March, 32 Organisation for Economic Co-operation and Development (OECD) nations agreed to release 400 million barrels of strategic petroleum reserves.Footnote 5

- Lower consumption. Global oil use dropped by about 2.3 million barrels per day in April, year over year.Footnote 6 "As gas prices rise, Asian governments in particular have recommended consumers take fewer business trips, work remotely and leverage alternative forms of transportation," Chiu says.

- U.S. economic and energy resilience. As a net oil exporter, the U.S. is helping to fill the Hormuz gap, with exports rising sharply since the war started to over 6 million barrels per day.Footnote 7

Moves for investors to consider

"For now, financial markets continue to price in a relative de-escalation in the coming months. But the longer the disruption lasts, the greater the risk of a larger hit to economic growth," says Chiu. "For investors, we continue to prefer the U.S. in portfolios because of its ability to remain resilient versus other economies."

Focus on the U.S.: An emphasis on high-quality U.S. stocks may offer a buffer from oil shocks, given U.S. energy self-sufficiency, while also positioning investors to potentially benefit from U.S. economic strength, record earnings growth and artificial intelligence capital expenditures in the long term. That said, it's important to stay disciplined and diversified across and within asset classes in the face of potentially volatile headlines, Chiu adds, and to rebalance during periods of volatility.

For latest insights from the CIO on the Iranian conflict and its impacts on the economy and markets, tune in to the

Market Update audiocast.

Footnote 1 CNBC, "The U.S.-Iran war is the biggest oil disruption in history," March 9, 2026.

Footnote 2 U.S. Energy Information Administration, "Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint," June 16, 2025.

Footnote 3 International Energy Agency, "Oil market report," Jan. 21, 2026.

Footnote 4 International Energy Agency, "IEA Member countries to carry out largest ever oil stock release amid market disruptions from Middle East conflict," March 11, 2026.

Footnote 5 International Energy Agency, "Oil market report," April 14, 2026.

Footnote 6 Bloomberg, "US oil exports hit record as Iran War energy crunch deepens", April 29, 2026.

Footnote 7 Bloomberg, "US oil exports hit record as Iran War energy crunch deepens", April 29, 2026.

May 13, 2026

Interest rates: Up, down or flat under new Fed chair?

Even as leadership of the Federal Reserve (the Fed) changes hands, persistent inflation may eliminate chances of hoped-for interest rate cuts through 2026. Kevin Warsh, confirmed by the full Senate on May 13, replaces Jerome Powell, whose term as chair ends on May 15. While the administration backed Warsh, a so-called interest rate dove favoring lower rates, as potentially more aggressive than his predecessor in pushing for cuts,Footnote 1 April inflation figures released yesterday show the Consumer Price Index up 3.8% from a year ago, well above the Fed's 2% target.Footnote 2

The case for current rate inaction

The latest inflation figures clearly present a challenge for the new Fed chair. Markets welcome interest rate cuts because they stimulate hiring and economic growth and make it easier for businesses and consumers to borrow money. "Yet while the labor market has softened, we haven't seen an increase in recent layoffs," says Matthew Diczok, head of Cross-Asset Market Strategy for the Chief Investment Office (CIO). "For the time being, this labor stability enables the Fed to focus on inflation pressures related to energy price spikes from the Iran conflict and tariff uncertainties, rather than unemployment."

Warsh would need to rally six other Fed governors to vote for a rate cut — a difficult task as long as these conditions persist, he adds. "Markets, in fact, no longer expect rate cuts this year. That's not necessarily a bad thing, as it highlights continuing economic resilience. Should inflation slow, as expected, it likely just pushes rate cuts into 2027." BofA Global Research, which had anticipated two cuts in 2026, now believes cuts may not come until mid or late 2027. A rate hike this year is considered unlikely.

The case for future cuts in the Warsh era

While interest rate expectations are always subject to change as economic conditions evolve, rising U.S. economic productivity may allow the Fed to accommodate an extended era of somewhat elevated inflation while maintaining or lowering interest rates to spur growth. Diczok points to the early 1990s, when the Fed allowed inflation to hover around 3.3% amid a tech-related productivity boom.

Today, productivity gains from artificial intelligence (AI) and other technologies are outpacing wage growth and supporting strong equity market performance, Diczok notes. "If productivity gains continue and we are able to work through the current energy crisis and get past tariff uncertainties, that would support the Fed's ability to resume rate cuts next year."

In the meantime, he adds, "fixed income investors with excess cash could consider

longer term bonds." In fact, he says, "even short-term maturities don't look bad right now." Relative to the rest of the world, U.S. Treasurys and Treasury Inflation-Protected Securities (TIPS) offer attractive inflation-adjusted yields and fixed income.

For latest insights on the markets, economy and where interest rates might go next, tune in regularly to the CIO's

Market Update audiocast.

Footnote 1 The Guardian, "US Senate expected to confirm Kevin Warsh as next Federal Reserve chair," May 11, 2026

Footnote 2 The Wall Street Journal, "Inflation soared to 3.8% in April, driven by gasoline prices," May 12, 2026.

April 29, 2026

Rate-decision repeat: Fed stands pat again

The Federal Reserve (The Fed) responded to current economic and geopolitical uncertainty by maintaining a wait-and-see approach at its April 29 meeting. In what may be its final meeting with Jerome H. Powell as chair, the Fed kept the federal funds rate at between 3.50% and 3.75%, as it has done since the start of 2026.

When could the cutting cycle resume?

"After three successive Fed rate cuts of .25% at the end of 2025, markets entered 2026 expecting additional cuts to help grow the economy," says Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank. Then geopolitics intervened. The Iran conflict generated waves of stock volatility, higher energy costs and fears of resurgent inflation.

More recently, a tenuous ceasefire brought lower oil prices and hopes that the conflict would wind down soon. "With labor demand soft and wage growth cooling, we still see room for two rate cuts later this year, especially if inflation remains contained," Hyzy says. "But everything depends on the economic data and continued de-escalation of the conflict."

Moving forward, rapid development of artificial intelligence (AI) could make those calls even tougher, he notes. A recent Capital Market Outlook article from the CIO, "

AI, Productivity, and R* (PDF)," suggests AI productivity growth could pressure rates upward even as AI-related job losses call for cuts.

A more immediate uncertainty: Who will sit as chair for the Fed's next rate decision, in June? Under Powell, whose second four-year term ends May 15, the Fed navigated pandemic-related economic crises and helped ease inflation from 9.1% in 2022 to 3.1% in February 2026. Yet its 2% inflation target has proved elusive, and the administration, criticizing Powell as too slow to cut rates, has nominated former Fed governor Kevin Warsh as his replacement. Powell has said he will hold his position until a new chair is confirmed.2

Ways to consider positioning your portfolio

"Over the long term, we believe the Fed's cutting cycle will continue, supporting growth in a U.S. economy that has proven remarkably resilient,"Hyzy says. This could create potential opportunities in the housing, financial and automotive industries, as well as small cap stocks, all of which tend to benefit from lower rates.

Fixed income investors could consider adding longer-term bonds to their portfolios to lock in current higher rates. (For more insights on what potential future rate cuts could mean for you, read

"Plan ahead to take advantage of Fed rate cuts.")But keep in mind that markets and investors are subject to the same uncertainties that are complicating the Fed's rate decisions. He adds, "The precise timing of Fed decisions matters less than keeping your portfolio diversified across and within asset classes and rebalancing after periods of volatility."

For more news and analysis, listen to our latest

CIO Market Update audiocast and check here for regular updates on the economy, the markets and where interest rates could be headed next.

POP QUIZ: How much power over rates does the Fed chair have?

Tap + to select correct answer and learn more

True or false: Decisions to increase, reduce or maintain interest rates are voted on by the 12 members of the Federal Reserve's Federal Open Market Committee (FOMC). The Fed chair, like the other 11, has only one vote.

True

Correct. That's correct. The voting members of the FOMC consist of the seven members of the Board of Governors, including the Fed chair, as well as the president of the New York Federal Reserve Bank and four other regional Reserve Bank presidents, who serve on a rotating basis. Each has only one vote. Split decisions can reflect differences in outlook about economic growth, inflation and the speed of rate hikes or cuts.

False

Incorrect. The voting members of the FOMC consist of the seven members of the Board of Governors, including the Fed chair, as well as the president of the New York Federal Reserve Bank and four other regional Reserve Bank presidents, who serve on a rotating basis. Each has only one vote. Split decisions can reflect differences in outlook about economic growth, inflation and the speed of rate hikes or cuts.

Footnote 1 PBS News, "Top Fed official sees potential rate hike amid higher gas prices, inflation concerns," April 6, 2026.

Footnote 2 The New York Times, "Powell says he will remain as Fed chair until successor is confirmed," March 18, 2026.

April 20, 2026

Will an inflation shock cause emerging markets to falter?

When investors hear "inflation shock," emerging markets (EM) might spring to mind, especially when the catalyst is geopolitical tension with implications for energy prices. The familiar concern: higher oil prices feed inflation, central banks tighten policy, growth slows and EM assets ultimately feel the pressure. But recent inflation dynamics among EM economies may be meaningfully different from past cycles.

The classic risk: energy prices and inflation pressure

A prolonged Middle East conflict could push global inflation higher through energy, commodity, and food prices. This scenario played out in early 2022, when an energy shock driven by the conflict in Ukraine sent inflation across many emerging economies into high single or low double-digit territory, triggering volatility and sharp policy responses in the form of rate hikes. Against that backdrop, it's reasonable to ask whether another oil spike could lead to a similar outcome.

A different starting point today

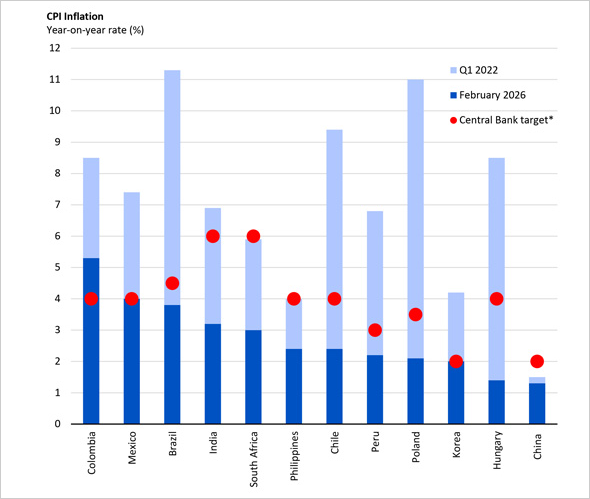

The comparison may be imperfect. Across many emerging economies, inflation is starting from a far more contained position than it was in early '22: Data analysis in the

Q1 2026 CIO Chart Book (PDF) shows that in several cases across EMs, Consumer Price Index (CPI) readings have been sitting below central bank targets, potentially reducing the risk of additional tightening even if energy prices spike further.

This CPI Inflation chart compares consumer price inflation across 12 countries at two points in time - Q1 2022 and February 2026 - and shows each country's central bank inflation target for reference. Colombia: Inflation was 5.3 percent in February 2026; 3.2 percent Q1 2022; Central Bank target at 4 percent. Mexico: Inflation was 4 percent in February 2026; 3.4 percent Q1 2022; Central Bank target at 4 percent. Brazil: Inflation was 3.8 percent in February 2026; 7.5 percent Q1 2022; Central Bank target at 4.5 percent. India: Inflation was 3.2 percent in February 2026; 3.7 percent Q1 2022; Central Bank target at 6 percent. South Africa: Inflation was 3 percent in February 2026; 2.9 percent Q1 2022; Central Bank target at 6 percent. Philippines: Inflation was 2.4 percent in February 2026; 1.6 percent Q1 2022; Central Bank target at 4 percent. Chile: Inflation was 2.4 percent in February 2026; 7 percent Q1 2022; Central Bank target at 4 percent. Peru: Inflation was 2.2 percent in February 2026; 4.6 percent Q1 2022; Central Bank target at 3 percent. Poland: Inflation was 2.1 percent in February 2026; 8.9 percent Q1 2022; Central Bank target at 3.5 percent. Korea: Inflation was 2 percent in February 2026; 2.2 percent Q1 2022; Central Bank target at 2 percent. Hungary: Inflation was 1.4 percent in February 2026; 7.1 percent Q1 2022; Central Bank target at 4 percent. China: Inflation was 1.3 percent in February 2026; 0.2 percent Q1 2022; Central Bank target at 2 percent.

This CPI Inflation chart compares consumer price inflation across 12 countries at two points in time - Q1 2022 and February 2026 - and shows each country's central bank inflation target for reference. Colombia: Inflation was 5.3 percent in February 2026; 3.2 percent Q1 2022; Central Bank target at 4 percent. Mexico: Inflation was 4 percent in February 2026; 3.4 percent Q1 2022; Central Bank target at 4 percent. Brazil: Inflation was 3.8 percent in February 2026; 7.5 percent Q1 2022; Central Bank target at 4.5 percent. India: Inflation was 3.2 percent in February 2026; 3.7 percent Q1 2022; Central Bank target at 6 percent. South Africa: Inflation was 3 percent in February 2026; 2.9 percent Q1 2022; Central Bank target at 6 percent. Philippines: Inflation was 2.4 percent in February 2026; 1.6 percent Q1 2022; Central Bank target at 4 percent. Chile: Inflation was 2.4 percent in February 2026; 7 percent Q1 2022; Central Bank target at 4 percent. Peru: Inflation was 2.2 percent in February 2026; 4.6 percent Q1 2022; Central Bank target at 3 percent. Poland: Inflation was 2.1 percent in February 2026; 8.9 percent Q1 2022; Central Bank target at 3.5 percent. Korea: Inflation was 2 percent in February 2026; 2.2 percent Q1 2022; Central Bank target at 2 percent. Hungary: Inflation was 1.4 percent in February 2026; 7.1 percent Q1 2022; Central Bank target at 4 percent. China: Inflation was 1.3 percent in February 2026; 0.2 percent Q1 2022; Central Bank target at 2 percent.Source: Bloomberg. Data as of February 2026. Latest data available. *Central bank inflation targets shown are the upper bound when set as a range.

This distinction matters because it is often the policy response — not inflation alone — that turns price shocks into growth slowdowns. "The starting point of lower inflation changes the equation," continues Sanfilippo. "Higher energy prices don't always equate to aggressive tightening for emerging markets."

A broader view on emerging markets

Despite elevated uncertainty, the overall growth and market outlook has not materially changed, and diversification across regions remains central to portfolio construction, Sanfilippo says.

She adds that in the CIO's view, EM performance today is a function of more than inflation alone. Currency trends, regional sector exposure, and long-term growth drivers matter just as much. EM Asia — now close to 80% of total EM market capitalization — is deeply connected to global technology supply chains and AI-related capital investment, while some commodity-producing markets can benefit from higher prices rather than suffer from them.

Revisit the CIO's outlook on emerging markets from earlier this year:

Video: Emerging Markets Outlook for 2026 Potential Opportunities

Press enter to play 'Emerging Markets Outlook for 2026 Potential Opportunities' video

On screen copy:

Chris Hyzy

Chief Investment Officer

Merrill and Bank of America Private Bank

On screen copy:

Please read important information at the end of this program. Recorded on 1/22/2026.

[Chris Hyzy faces the camera and speaks directly to the audience. The shot then pans to a conversational discussion between Chris and Lauren Sanfilippo.]

Chris Hyzy

Hi, I'm Chris Hyzy, chief investment officer for Merrill and Bank of America private bank. Today, we're looking at one of the most notable shifts in our outlook for 2026.

On screen graphic:

Emerging markets showing momentum:

Strong 2025 performance

Broadening global expansion

Apparently overvalued dollar

Which is a more positive stance on emerging markets, a strong 2025 performance, a broadening global expansion, and a dollar that appears overvalued are contributing to this shift, along with tailwinds including potential lower interest rates and easing of oil prices. With capital rotating back into emerging assets, now is potentially a pivotal time to assess EM in your portfolio. What's behind these trends and what do they mean for investors?

On screen copy:

Lauren Sanfilippo

Senior investment strategist

Chief Investment Officer

Merrill and Bank of America Private Bank

Joining me now is senior investment strategist Lauren Sanfilippo to break it all down. Lauren, welcome.

Lauren Sanfilippo

Hi, Chris.

Chris Hyzy

We're going to start at the top. We have this concept called what's rare this year. What's rare in terms of growth around the world. Whether it's the US potentially above 5% nominal growth around the world collectively 6% at a time where short interest rates in the states are coming down. Typically, when you see geopolitical activity rise, you get a stronger dollar, not a weaker dollar like we've seen recently. There's a lot of rarities out there. Let's start with the emerging markets and let's go into what is different with the emerging markets within the context of what just happened in 2025.

On screen copy:

Emerging markets returned 34% in 2025, outperforming the S&P 500 by 16 points.

Source: Bloomberg data from MSCI Emerging Markets and S&P 500 Indexes.

Past performance is no guarantee of future results.

Lauren Sanfilippo

What's rare is that the emerging markets actually outperformed almost put up double the performance that the US did last year. And so in that sense, we're coming into the year already with markets a little bit hot. And so I think the set up is a little bit rare this year. It's just a story of chronic underperformance from the emerging markets. But a lot of the forces now have aligned. Whereas global growth, is narrowing. The divergence is narrowing between the rest of the world and the U.S., that's one.

On screen copy:

Global growth expected to reach 3.4% in 2026.

Source: IMF World Economic Outlook Update, January 2026

Earnings momentum looks good for emerging markets. And we have global trade that's reaccelerating. So there's a lot of good things that are happening that are rare in a sense for emerging markets.

Chris Hyzy

When bucket the emerging markets all together, we can't look away from the fact that overwhelmingly large part of the index is China. We'll get there in just one second. But when we put all of the emerging nations together as an asset class, what type of earnings growth are we expecting? Is it above what the US can potentially create for all of 26?

Lauren Sanfilippo

Yeah. You know it's roughly in line with the US but just different factors right. So whereas in the US we're looking at earnings that instead of it just being powered by seven tech companies, hyperscalers overwhelmingly their earnings growth is decelerating. And we're seeing the broadening from the 493 come up behind that tech sort of earnings outperformance that we've seen in recent years. Now for EM the story is a little bit different right. And some of those earnings trends just look really good. You're looking at for example the tech-oriented economies in markets, right, that we think are very compelling opportunities in 2026.

Chris Hyzy

Let's talk about China. A few years ago, China technology segment of China itself kind of went to the wayside a little bit. We didn't really talk about it, even though they were building this so-called dominance or at least race for dominance against the US. And then all of a sudden, they're supportive. There's particular government expenditures that are supportive of China technology in general. But also we're starting to hear about other stimulus with the consumer. Is that a contributing factor to being overweight the emerging markets?

On screen copy:

China represents 27% of the MSCI Emerging Market Index.

Source: Factset, as of 1/22/2026

Lauren Sanfilippo

There's a lot going right in China now where that that wind is really changed. Right. And it's 27% of the EM index. And so this is a weight that matters. It's a little bit similar in, in Latin America, actually. Different EM here in the sense that Mexico takes up a lot of that index. And so concentration is a risk.

Chris Hyzy

You talked about earnings growth. We talk about valuation in the United States of being at a premium. What's the valuation like collectively in the emerging markets.

On screen copy:

Emerging market equities offer attractive valuation multiples vs. U.S.

Lauren Sanfilippo

Yeah. So actually valuation is a compelling opportunity in emerging markets. And you know where there's been concerns over AI. Maybe these valuations got a little bit lofty for some investors here in the US. You can actually look for those opportunities abroad at valuations that could be more attractive right. So I'm talking about tech oriented markets such as Korea, Taiwan even China. And so that's what we're looking at for this year.

Chris Hyzy

There's been a lot of changes politically in the emerging markets over the years. It seems to be relatively calm right now. When we think about an active way to think about the emerging markets, is geopolitical risk still one of the bigger risks out there as it relates to the direction of asset prices?

Lauren Sanfilippo

Geopolitical risks are very much so part of the equation this year. We've seen what's gone on just year to date, right? In the few trading weeks that we've had.

Chris Hyzy

Feels like a half a year already.

On screen copy:

Supreme Court ruling on Trump administration tariffs could affect EM outlook.

Lauren Sanfilippo

For sure. And in front of us is still the IEEPA Supreme Court ruling the emergency powers over the tariffs. So trade and tariff frictions very much part of the story this year still. Right. That unfortunately didn't go away with 2025.

On screen copy:

Dollar-based investors are significantly underweight in emerging markets assets.

Chris Hyzy

One of the great benefits, at least right now, could potentially be the fact that dollar based investors are significantly underweight, emerging assets in general, emerging equity assets partially on the debt side as well. And with money flow, what other drivers are you thinking about with reallocation?

Lauren Sanfilippo

The dollar we see is still weakening this year right. Nothing like the 7% on a trade weighted basis dollar decline we saw last year, which primarily took place in the first half of the year. We foresee for this year still a softening in the US dollar. And so that would be a contributor and accretive to emerging markets.

Chris Hyzy

That's a very good point, because if you get the weaker dollar you get earnings growth, you get global growth going up. What tends to follow is natural resource prices also rallying, which we have seen in some cases not just precious metals but base metals and other parts of the natural resource spectrum is that is what is expected as well in 26.

Lauren Sanfilippo

Yeah. And I think you could also see like some of the industrial uses for some of those metals. Right. That's actually an attractive investment opportunity I think for us this year, particularly looking at Latam, just as a region that would probably benefit from that.

Chris Hyzy

Lauren we talked about earnings growth and valuation. Some other factors. Years ago for many decades frankly there was a high correlation to rising oil prices with enthusiasm, particularly as relates to Latin America within emerging markets. Do oil price direction matter just as much today as it did in the past. Or is there a different approach.

Lauren Sanfilippo

Different in the sense that China's growth model has changed a little bit, where it felt like in years prior is more like boom bust. Depending on what's happening in the commodity landscape, sort of what's happening in China, right. And vice versa. Now it's a lot different in the sense that China has actually tried to become more consumption based. Right. And so they're moving towards us. It's happening slowly. I mean, it did print on 1.2 trillion dollar trade surplus last year. And so they're still very much export oriented, but they are moving towards a more consumption based model.

Chris Hyzy

So an overall more diversified approach as to what is driving the enthusiasm over the emerging market landscape.

Lauren Sanfilippo

That's right.

Chris Hyzy

What are we missing? We talked about geopolitical risks. Is there anything else top of mind that you might be guarded about for us to watch for as it relates to emerging markets in general?

On screen copy:

Potential emerging markets downside scenario: global growth scare.

Lauren Sanfilippo

Yeah, I mean, maybe a global growth scare. It's all these things that we would probably factor in that just aren't right now factored into our models and assumptions. Right. So there are certainly things that could take place. But the overarching idea is that in Em would be sort of like any allocation would be a sleeve in the portfolio, right? In the sense that while this has been a great conversation about emerging markets, we have that US bias. And that's the core of the portfolio. So this would just be a little bit of a bolt on. Right. The diversified sort of aspects to a portfolio.

Chris Hyzy

Something that a dollar-based investor hadn't had to think about for a very long period of time.

Lauren Sanfilippo

Or wasn't able to.

Chris Hyzy

Great point. Lauren, I want to thank you for joining me today.

Lauren Sanfilippo

Thank you so much.

[The shot transitions back to just Chris on camera speaking directly to the audience.]

Chris Hyzy

Emerging markets are clearly an important part to consider for a balanced portfolio in 2026 and beyond. Alongside other shifts in asset classes and sector positioning. For guidance tailored to your long term goals, connect with your advisor, if you work with one, in order to see how these trends could work for you. I'm Chris Hyzy, thanks for watching and we'll see you next time.

On screen disclosures:

Important disclosures

The opinions expressed are as of 1/22/2026 and are subject to change.

Investing involves risk. Past performance is no guarantee of future results.

Asset allocation, diversification, and rebalancing do not ensure a profit or protect against loss in declining markets.

Investments have varying degrees of risk. Investing in emerging markets may involve greater risks than investing in more developed countries. In addition, concentration of investments in a single region may result in greater volatility. Investments in emerging- and frontier-markets securities may be subject to greater market, credit, currency, liquidity, legal, political and other risks compared with assets invested in developed foreign countries.

This information should not be construed as investment advice and is subject to change. It is provided for informational purposes only and is not intended to be either a specific offer by Bank of America, Merrill or any affiliate to sell or provide, or a specific invitation for a consumer to apply for, any particular retail financial product or service that may be available.

The Chief Investment Office (CIO) provides thought leadership on wealth management, investment strategy and global markets; portfolio management solutions; due diligence; and solutions oversight and data analytics. CIO viewpoints are developed for Bank of America Private Bank, a division of Bank of America, N.A., ("Bank of America") and Merrill Lynch, Pierce, Fenner & Smith Incorporated ("MLPF&S" or "Merrill"), a registered broker-dealer, registered investment adviser and a wholly owned subsidiary of Bank of America Corporation ("BofA Corp.").

Merrill makes available certain investment products sponsored, managed, distributed or provided by companies that are affiliates of BofA Corp. MLPF&S is a registered broker-dealer, registered investment adviser, Member SIPC and a wholly owned subsidiary of BofA Corp.

Merrill Private Wealth Management is a division of MLPF&S that offers a broad array of personalized wealth management products and services. Both brokerage and investment advisory services are offered by the Private Wealth Advisors through MLPF&S. The nature and degree of advice and assistance provided, the fees charged, and client rights and Merrill's obligations will differ among these services. The banking, credit and trust services sold by the Private Wealth Advisors are offered by licensed banks and trust companies, including Bank of America, N.A., Member FDIC, and other affiliated banks.

Bank of America Private Bank is a division of Bank of America, N.A., Member FDIC and a wholly owned subsidiary of BofA Corp. Trust and fiduciary services are provided by wholly owned banking affiliates of BofA Corp., including Bank of America, N.A.

Investment products:

| Are Not FDIC Insured |

Are Not Bank Guaranteed |

May Lose Value |

© 2026 Bank of America Corporation. All rights reserved. 8734056 - 01/2026

[End of transcript]

What this means for portfolios

The CIO continues to view EM equities as offering attractive valuations with improving longer-term fundamentals, even as near-term volatility persists. But, Sanfilippo cautions, emerging markets are no longer a single, uniform story. Inflation and energy risks vary by region, with parts of EM Asia benefiting from technology and AI investment, and some commodity-oriented economies gaining from higher prices. We believe the takeaway for clients is straightforward: consider staying anchored to your EM allocation and using bouts of volatility to rebalance, rather than reacting to short-term swings in oil prices or geopolitical headlines.

March 18, 2026

Understanding the latest Federal Reserve rate pause

Amid mixed signals on jobs and inflation, the Federal Reserve (the Fed), as widely expected, held steady on interest rates at its March 18 meeting. The decision, which leaves the federal funds rate at between 3.50% to 3.75%, marks the second pause in 2026, following three consecutive rate cuts to close out 2025.Footnote 1

Why the pause?

The economy's surprising loss of 92,000 jobs in FebruaryFootnote 2 might have argued for an additional rate cut to stimulate hiring. But surging oil prices since the Middle East conflict started on Feb. 28 have raised concerns that stubborn inflation could reignite — the Fed typically fights inflation by raising rates to cool the economy. "The Fed is walking a fine line between its goals of maximum employment and moderate inflation," says Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank.

What's next for the economy and rates?

"While some observers have warned of 1970s-style stagflation, when prices rise while the economy sputters, that's not our base case," Hyzy says. "U.S. energy production has made the economy more resilient against oil shocks. And the economy, despite some concerns, remains fundamentally strong." In addition, Hyzy says, "We expect the current rate-cutting cycle to resume later this year, but the pause will likely continue until the Fed has greater clarity on where the Middle East conflict, and inflation, are headed."

How can investors respond?

Investors might take a page from the Fed's playbook by remaining patient and avoiding hasty responses to geopolitically driven volatility, Hyzy advises. "Stay diversified across asset classes and invest with long-term goals in mind," he adds. "Periodically rebalance and look at temporary declines as potential opportunities to add to your portfolio."

Footnote 1 The New York Times, "Federal Reserve Leaves Interest Rates Unchanged," March 18, 2026.

Footnote 2 U.S. Bureau of Labor Statistics, "Employee Situation Summary," March 6, 2026

March 10, 2026

Navigating a new world of uncertainties in 2026

A war-related spike in oil prices drove sharp volatility in stocks as markets opened for the week of March 9.Footnote 1 Oil briefly topped $100 barrel — 40% higher than before the U.S. and Israel launched missile attacks on Iran on Feb. 28Footnote 2 — raising fears over broader economic impacts if the war widens and drags on. And the Middle East is just one of many concerns in a year of uncertainties. "Investors should expect elevated volatility in the months ahead," says Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank. "At the same time, it's important to stay focused on the underlying forces driving long-term growth."

Seeking signs of stability

In addition to oil prices and stock volatility, the Chief Investment Office will be watching several key market factors in the coming weeks for signs that conditions are stabilizing, Hyzy says. For example, credit spreads (the difference in yield between corporate bonds and U.S. Treasurys of similar duration) have been widening — often a sign of investor concern about the economy. "We're also closely following inflation, the strength of the U.S. dollar, and bond yields and rates, all of which should help dictate what's ahead for asset prices in the short and medium term."

Tracking other uncertainties

Even without the Middle East conflict, other pressures have the potential to jolt investors and markets in 2026. One example: "Midterm elections, coming in November, typically bring higher-than-normal volatility," Hyzy says. Among the other possible contributors to volatility: the impact of artificial intelligence on the software industry, stresses in the private credit market, the partial government shutdown and its potential impact on the travel industry, the impact of tariffs, and more.

Keeping a long-term focus

While an extended war and persistently high oil prices present risks for the global economy,

historically geopolitical events of this nature have had limited long-term impact, Hyzy notes. And the U.S., as a leading energy producer and net exporter of oil, may be less vulnerable than other regions to oil shocks, he adds. As for the other uncertainties, the volatility they may create, while unsettling, will likely be temporary, Hyzy believes. For example, "despite the volatility midterm elections cause, markets historically have hit new highs a year later," he adds.

"Given all the uncertainties, there's no clear timetable for market stabilization," Hyzy says. "We continue to emphasize patience, a balanced, diversified approach, and having a detailed plan to buy or rebalance on weakness." He advises long-term investors to avoid trying to "time" markets and instead stay focused on broader trends such as corporate earnings growth, rising capital investment, productivity, accelerated innovation and global economic growth.

Footnote 1 NBC News, "Oil hits $100 per barrel for first time since July 2022," March 8, 2026.

Footnote 2 Reuters, "Iran war boosts oil price, but oil major shares are stuck on the sidelines," March 9, 2026.

Share:

Important Disclosures

Investing involves risk, including the possible loss of principal. Past performance is no guarantee of future results.

Opinions are as of the date of these articles and are subject to change.

Bank of America, Merrill, their affiliates, and advisors do not provide legal, tax, or accounting advice. Clients should consult their legal and/or tax advisors before making any financial decisions.

This information should not be construed as investment advice and is subject to change. It is provided for informational purposes only and is not intended to be either a specific offer by Bank of America, Merrill or any affiliate to sell or provide, or a specific invitation for a consumer to apply for, any particular retail financial product or service that may be available.

The Chief Investment Office (CIO) provides thought leadership on wealth management, investment strategy and global markets; portfolio management solutions; due diligence; and solutions oversight and data analytics. CIO viewpoints are developed for Bank of America Private Bank, a division of Bank of America, N.A., ("Bank of America") and Merrill Lynch, Pierce, Fenner & Smith Incorporated ("MLPF&S" or "Merrill"), a registered broker-dealer, registered investment adviser and a wholly owned subsidiary of Bank of America Corporation ("BofA Corp.").

BofA Global Research is research produced by BofA Securities, Inc. ("BofAS") and/or one or more of its affiliates. BofAS is a registered broker-dealer, Member SIPC, and wholly owned subsidiary of Bank of America Corporation.

All recommendations must be considered in the context of an individual investor's goals, time horizon, liquidity needs and risk tolerance. Not all recommendations will be in the best interest of all investors.

Investments have varying degrees of risk. Some of the risks involved with equity securities include the possibility that the value of the stocks may fluctuate in response to events specific to the companies or markets, as well as economic, political or social events in the U.S. or abroad. Bonds are subject to interest rate, inflation and credit risks. Treasury bills are less volatile than longer-term fixed income securities and are guaranteed as to timely payment of principal and interest by the U.S. government. Investments in a certain industry or sector may pose additional risk due to lack of diversification and sector concentration.

Investments in foreign securities involve special risks, including foreign currency risk and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are magnified for investments made in emerging markets. There are special risks associated with an investment in commodities, including market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes and the impact of adverse political or financial factors.

Income from investing in municipal bonds is generally exempt from Federal and state taxes for residents of the issuing state. While the interest income is tax-exempt, any capital gains distributed are taxable to the investor. Income for some investors may be subject to the Federal Alternative Minimum Tax (AMT).

Retirement and Personal Wealth Solutions is the institutional retirement business of Bank of America Corporation ("BofA Corp.") operating under the name "Bank of America." Investment advisory and brokerage services are provided by wholly owned non-bank affiliates of BofA Corp., including Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as "MLPF&S" or "Merrill"), a dually registered broker-dealer and investment adviser and Member SIPC. Banking activities may be performed by wholly owned banking affiliates of BofA Corp., including Bank of America, N.A., Member FDIC.

You have choices about what to do with your 401(k) or other type of plan-sponsored accounts. Depending on your financial circumstances, needs and goals, you may choose to roll over to an IRA or convert to a Roth IRA, roll over a 401(k) from a prior employer to a 401(k) at your new employer, take a distribution, or leave the account where it is. Each choice may offer different investments and services, fees and expenses, withdrawal options, required minimum distributions, tax treatment (particularly with reference to employer stock), and provide different protection from creditors and legal judgments. These are complex choices and should be considered with care.

Diversification does not ensure a profit or protect against loss in declining markets.

Investing in Gold involves special risks, including market price fluctuations, regulatory changes, interest rate changes, credit risk, economic changes, and the impact of adverse political or financial factors.

Equity securities are subject to stock market fluctuations that occur in response to economic and business developments. Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. Investments focused in a certain industry or sector may pose additional risks due to lack of diversification, industry volatility, economic turmoil, susceptibility to economic, political or regulatory risks and other sector concentration risks.

MAP9052898-02052028